Hello everyone!

Nvidia reported earnings yesterday and is up nearly 10% after hours, bringing the company's market cap to 545b and the valuation to 120x P/E and 20x P/S. In my opinion, it is the most overvalued stock in the market right now.

Earnings and the Trend

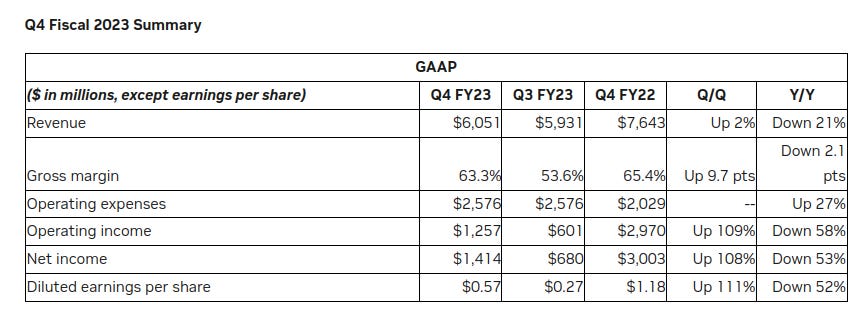

The market cheered on Nvidia using so many "AI" buzzwords in their earnings call and that they beat their extremely lowered expectations. By all accounts, these earnings would be terrible for any company, let alone one that is priced to perfection. Operating income down 58% is brutal. But if you look closer, it looks even worse. Data center chips are up 11% YoY (which is too little, as I will show), but they are down 6% QoQ - meaning they have the first deceleration in earnings here since Q1 2021. Funnily enough, the data center increase is less than the increase on cereal YoY. (thanks, @BluthCapital, for the info)

At the same time, the company has big SBC (share-based compensation) expenses. For the full year it was close to 50% of net income, in the last quarter it was 68% of operating income. Terrible for a company as mature as Nvidia.

Gaming has been down 46% a year and up and up 16% QoQ. The downfall has been caused by the decline of crypto, the switch from Ethereum to Proof-of-Stake needing less processing power and the general decline in gaming as countries have opened up after the pandemic. At first glance, a small recovery looks like good news. Well, not exactly. Inventory is up 98%, but what is worse is that they released the RTX 4000 series. Gamers have been starved for graphics cards for a long time, with the exception from 2018-2019, due to the high demand of crypto miners driving up prices. Now cards are available, yet it seems demand is not really recovering. As a comparison for the RTX 2000 series release, the companies recorded over 67 and 106% YoY growth and 10% and 11% QoQ respectively.

Forward guidance

But forward guidance cry the bulls!

The CFO guided towards 6.5b in revenues with 64.1% gross margins and 2.53b in operating expenses, bringing us to 1.63b in operating income. That certainly looks better than the current quarter, the problem is that it is still a decline compared to last year.

In Q1 2022 (which is Q1 2023 for Nvidia's fiscal year), the company had revenues of 8.2b and operating income of 1.8b. The guidance is 21% lower in revenues and 13% lower in operating income than in the last year. So much for a "growth stock". Btw, YoY the stock is down less than 5% despite earnings eroding 50%+.

But AI

Well, the AI hype is certainly there. The thing is: it won't accelerate the growth by a lot. Their data center offerings have been used for years now to train Neural Networks and AI. Their cloud computing (now AI Cloud Computing instead of GPU cloud computing because that is better), will grow - but not significantly more than it already did. Furthermore, the companies that try to hype up their stock on AI, did the same with the metaverse and bought GPUs for that. These can be used for more than to render graphics.

Demand will certainly grow as the processing power demands continue to rise, but not in an explosion like the market currently expects. Nvidia is also the biggest player in the space.

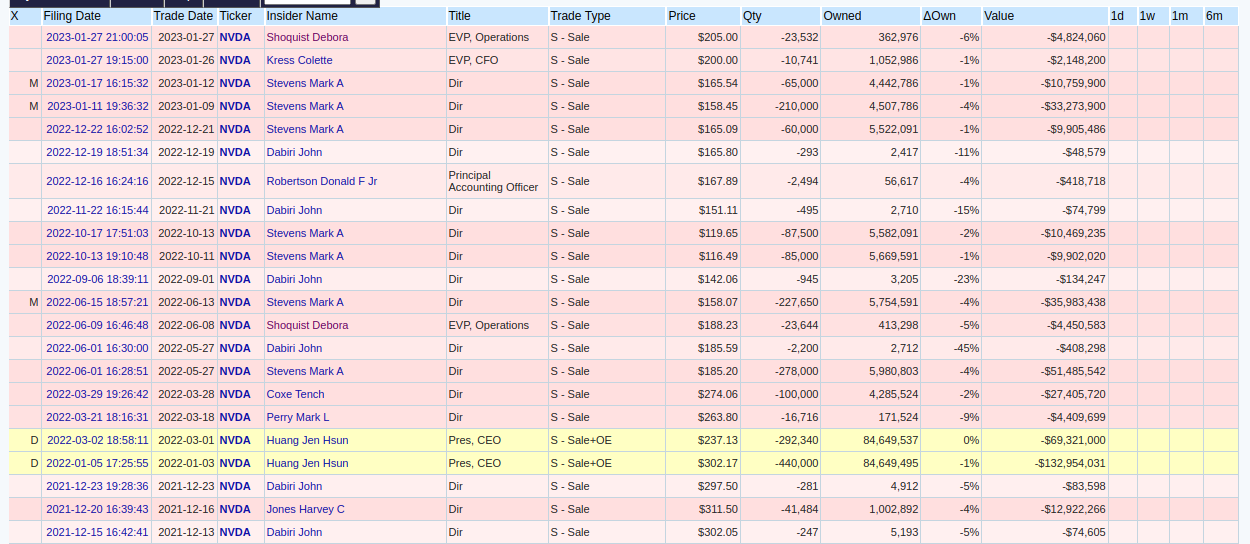

Insiders have also been selling like madmen at prices much lower than today.

Cisco

The current valuation leaves Nvidia more expensive than it was at its peak in 2021 when the company was growing 50%. The company reminds me now of Cisco during the dotcom bubble. Great companies, just insanely overvalued. Cisco declined 38% before rallying back to 38% and subsequently dropping 80%. Nvidia dropped 68% and is now up 115% since the lows. History doesn't repeat, but it does rhyme. For Cisco, it was also said that the company would grow based on the Internet hype, but once demand was met, their earnings plummeted - just like we are seeing now with Nvidia. The market doesn't accept that yet, but being patient is required.

I would say that Google's business model is much better than Nvidia's. If Nvidia had the same multiple as Google, it would trade at around $50 per share, not $222.

There are also only two companies since 1999 who had a positive return, with a P/S ratio of over 15 and being in the top 10 worldwide market caps. Alibaba and Facebook. Both during a 0% interest environment and the full force of internet adoption behind them.

What is baked into that valuation

At 120x P/E the market certainly expects growth in the next 10 years. Now, valuations should already compress due to interest rates rising, but I will compare it to the market. Let's assume that both the market and Nvidia trade at 20x P/E after 10 years. Mature chip companies usually are around 10x earnings, but we put a premium on Nvidia.

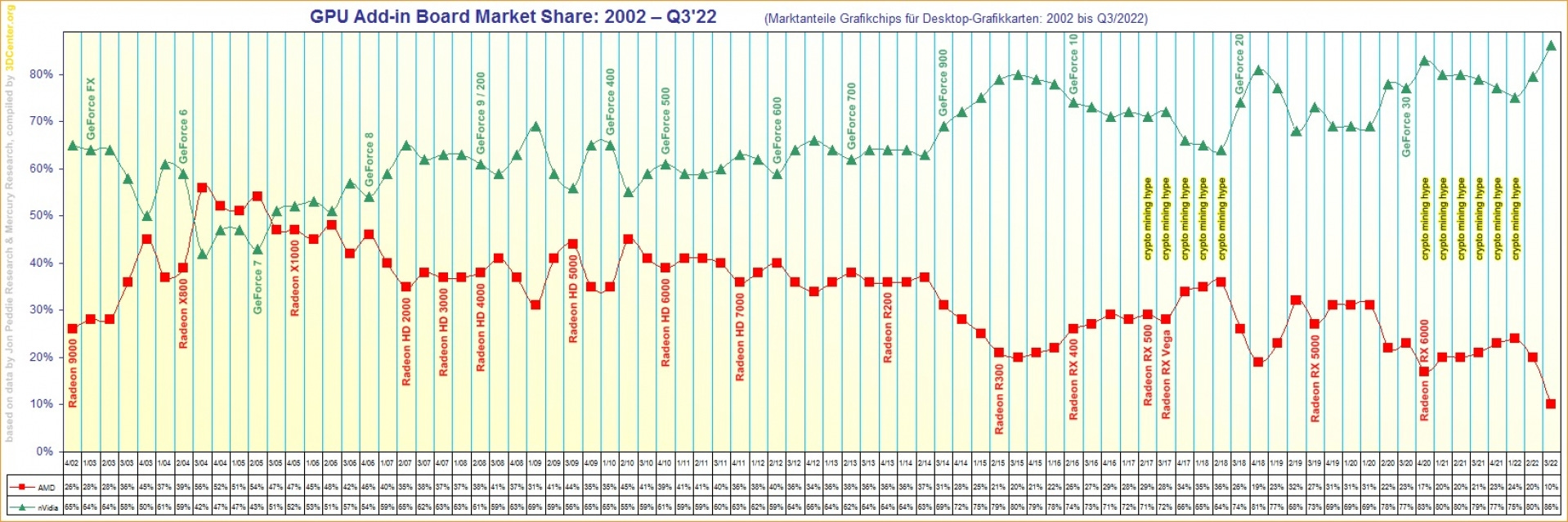

Historically, the market has returned 10% a year, that will be our baseline. Now the CFO guided towards lower earnings in Q1, but let's assume that in 2023 the company will grow 10%. That means that the company needs to grow around 30% for nearly a decade to get the same return as the market. Nvidia, in contrast to AMD, also has the problem, that they are already the biggest player in that space. In Q3 2022, Nvidia had an 86% market share for GPUs in desktop computers.

The company is also completely dominant in enterprise GPUs. According to IDC, Nvidia held 91.4% of the enterprise GPU market.

The bet is not only that they will keep their huge market share - despite big companies like Google, Microsoft and Amazon being in the process or already releasing data-center chips - and that the market will expand by a huge amount each year.

Technicals

On a technical standpoint, the company is moving against huge resistance at the 229 level. Since the end of January, the company trades in the range of 209-230, which it did previously before the big run up in October 2022, in March 2022 before the bear market rally and in April before a nearly 50% decline. If the stock doesn't manage to stay above the 209 in the next following days, it is very likely to drop by a lot. The next big support line is around 140. In terms of oscillators those show to a sell, while the moving averages show a slight buy. So other than the resistance levels, the technicals are not giving us a strong signal in any direction.

I think that similar to the earnings reactions of Coinbase and Doordash, it goes up 10% and then drops and closes red at the end of the day. If it does close significantly under 209, it could mean that the rally of the last 6 months is over. The market is irrational tho, so who knows what will happen in the short term.