Hello!

The market is in turmoil with the regional bank news and the UBS/Credit Suisse take-over. Today is gonna be a long one:

Learning from Leucadia

Learning from Victor Niederhoffer - a great failed trader

The Shitco Index

Future of the newsletter - why I will never go full paid.

Nvidia Update

In my last article I wrote about Nvidia being the most overvalued stock of the market. Well it got even more overvalued and instead of being 545b market cap, it is now 680b. AMD has a market cap of 155b, so the increase is close to 90% of AMD. Well it is highly irrational but it will take a while to come down due to the AI hype. What is more surprising is that the bankruptcy of Silicon Valley Bank did not spark a sell-off in tech. Just like electronic companies in the 60s or Internet companies in the 2000s - the biggest customers of tech companies are tech companies. The loss of confidence in the VC area will lead to lower funding and less money flowing into tech stacks. Add that interest rates are now higher, and that the bank that used to lend to start-ups and unprofitable tech companies is now gone, and suddenly capex into tech is much lower. Despite the AI hype, I believe that Nvidia's Q2 will be weaker than they expect. It will take some time before my thesis plays out. Given that fund flows will now redirect from banks to the "safe" tech sector, it might take even longer.

There are also now copy cats of the ChatGPT. While these are not as sophisticated, most AI in my opinion will be specialised. For example for lawyers trying to find court cases, precedents and laws quickly and to create drafts. The big news is that it was trained on a single RTX 4090 in less than five hours. That means that you don't need as many graphics cards as the market is letting us believe to train a proper model. The RTX 4090 is a consumer card, and while expensive with around 2000$ much more affordable then something like the H1 that is around $30,000. While demand for graphics cards will obviously rise, improved efficiency usually slows the growth prospects. Since Nvidia needs 30% growth for a decade to justify their valuation, that isn't great news.

Other thoughts

I looked through the obscure stocks I wrote about, and didn't find one that was appealing to me.

What really grinds my gears is when someone says that he missed stock X as he bought it in the past and then sold - and it then went up a lot more. In my opinion there are no errors of omission. The market gives you opportunities every day.

If you sold X because it went against your investing framework (whether that is value investing or something else), it wasn't a mistake. If you sold X because you were fearful and would have held it in your framework, you probably had a long time to correct that mistake. If you still didn't correct that mistake, one needs to work on how to implement the framework better.

Learning from Leucadia

Leucadia was a great company, built on a deep value investing framework. Here are the letters from 1978-2012. From 1979-2012 they compounded with 19% CAGR. What is more remarkable is that from 1978 to 1992 they had a CAGR or 47%, which declined mainly due to the increasing size of the company.

This was their mantra:

We tend to be buyers of assets and companies that are troubled or out of favour and as a result are selling substantially below the values which we believe are there. From time to time, we sell parts of these operations when prices available in the market reach what we believe to be advantageous levels. While we are not perfect in executing this strategy, we are proud of our long-term track record. We are not income statement driven and do not run your company with an undue emphasis on either quarterly or annual earnings. We believe we are conservative in our accounting practices and policies and that our balance sheet is conservatively stated

They also repeatedly underline the importance of not overpaying for assets. Another point is that there are no value traps in excellent assets. If they are truly great they will appreciate it.

In contrast to Ben Graham, Leucadia was quite concentrated - at least in the early days. Then it bought what was cheap, no matter the industry. From gold miners to bolivian bonds and everything in-between. For me flexibility is one of the hallmarks of a great investor and they obviously were.

Lessons from Victor Niederhoffer - a great failed trader

Victor Niederhoffer is a fascinating character. He went from doing 30% for 20 years using futures, stocks and currencies to bankruptcy. By betting on Thai banks during the Asian Financial Crisis in 1997 and then selling put options on the NYSE, he blew up after the market declined 7% in a day. Losing over 50m of his own personal fortune he had to auction off his silver and art collection. He started anew, being again in the top performing funds from 2001 to 2006 before blowing up again in 2007 - being at the wrong end of the subprime mortgage crisis. Many would dismiss him as an investor/speculator/trader, but I think you can learn from nearly everyone. Here is a great documentary and here is a good article.

He published two books, "Education of a speculator" and "Practical Speculations" of which I will summarise interesting lessons or opinions. His investment style was trying to spot patterns and statistical anomalies in the market and then speculating on them. He usually back-tested his ideas and tried to apply the scientific method to it.

Education of a speculator is a weird book, where he relates the markets to squash, music and everything that comes to mind. There are some great pieces of wisdom in it, but it is a tough read.

Beginnings

Starting trading Victor Niederhoffer got lucky. In eighteen months he ran fifty thousand dollars up to twenty million. He thought there was going to be inflation and kept selling treasury bonds, buying gold and silver. That worked well, until one day during a game of racquetball he called to see where the market was. In an hour the gold price fell immensely, halving his net worth. As he saw a lot of gamblers die broke - he had a system. He told his assistant and later wife "If I ever lose more than half my stake, close out all my positions". During the second game she sold everything. The brokerage account was now worth just 5 million, but at least he got out with that much.

Sadly he did not adhere to his own advice in 1997.

Avoid disaster

There are many ways to lose, but only a few ways to win. The best way to victory is to master all the rules for disaster and concentrate on avoiding them.

This is a very similar approach to Charlie Munger, who often inverts the problem to find a good solution.

Furthermore Niederhoffer says that you should not pyramid into losses and that shorting a stock is a lesson for disaster. However by selling puts, he was effectively short volatility and blew up.

You are in the greatest danger when your game appears the safest

Education of a speculator

He wrote that given the amount of trades he did, and his average profit it is 700 std. deviations from random. As a result he doesn't think it was luck. I agree. Reading through both of his books, it wasn't luck - which shows that you can still easily blow up being in the wrong positions.

Niederhoffer was always emotional about his trades. He often couldn't talk about the market declining as it was too painful. He was a partner of George Soros, who always was calm. Soros said that the market is open again the next day, and there are plenty of opportunities to make back the losses.

One thing that he says most traders do wrong is to take small gains, instead of letting them run and then closing them once they reverse course. This is then often not enough to cover the losses. I agree and have the same problem. I often close out investments way too early, and miss a large gain.

Practical Speculation

In practical speculation Victor challenges conventional thinking such as PE ratio being indicative of returns or that if the combined earnings of the market go up - that stocks should go up as well. I found those views rather refreshing. He makes the point that the market is more likely to go down the year of good earnings rather than up. The data of this book only goes to 2002, but it makes sense. The market prices in future expectations. So when the earnings go up, the market has often already priced that in. However for individual stocks the conventional wisdom of higher earnings = higher stock price still holds true.

Technical analysis and trend following doesn't work

After back-testing hundreds of indicators and patterns, not one was reliable. This is no surprise. In my opinion technical analysis can't forecast the future and should be used as additional information similar to a ratio like P/B. It is additional information about what the market has thought in the past about the stock.

Furthermore trend following was not proven to work, rather the opposite was true. It is more likely that the performance was bad in the second half of the year if it was good in the first half. The market also often rallies when gloom is the greatest. That a rally was coming is always obvious after the facts. When Vix goes over 35 the following days are usually positive - and when it is under 20, they are usually negative. When I back-tested it, it was 52% profitable with a profit factor or 1.4 for the market. With 52% I am not sure if it is a good signal or if it isn't.

Boasting and Stadium deals

In a back-test companies where the CEO boasts that they are leaders in their field under-performs. Whereas CEOs that are described as low key, down-to-earth, modest and unassuming usually outperform. Their returns were seven times that of the market in 15 years.

Companies and countries that complete tall, lavish buildings usually experience disaster shortly thereafter. That was true in Babylon, Kuala Lumpur in 1997 or the Nasdaq MarketSite Tower before a 70% decline. Enron's lavish tower was close to completion when it filed for bankruptcy.

Companies whose CEO appears on Forbes also tend to perform about 5% worse than the market in the month after making the cover. The Stadium jinx has been widely noted with Enron, TWA; CMGI, 3Com and more recently FTX. During the year of naming and the subsequent year, the companies performed significantly worse than the S&P 500. In the second and third year however the results are mixed to bullish.

Criticism of Benjamin Graham.

Niederhoffer dismisses Graham, as Geico that went against his principles was the best investment. He also concluded that many imitators and funds do poorly. He also reasons that growth stocks over-performed value stocks from 1965 to 2002. While value outperformed in the consequent decade, we have just experienced another decade of huge returns for growth.

My problem with the criticism of Graham is that : First. Nearly all funds do poorly, so it is likely for value investing funds to do so as well. Second, is that the back-test of net-nets has done spectacularly. However this strategy is not feasible for funds, as the companies are often so small you would move the market with a big fund. That is also the reason why Buffett switched from special situations and cigar butts to buying great companies at fair prices, despite him having outstanding returns.

Things to keep in mind

There are a few things that Victor keeps in mind when buying stocks.

Stocks have a CAGR of 7-10% over the long run.

Insider buying and selling are great at timing

The higher a company’s expected growth rate, the higher the current price relative to current earnings.

As much as 80 percent of the maximum risk reduction can be achieved with as few as 15 stocks.

In most periods, small companies tend to perform better than big companies.

Companies that made buybacks / dividends tend to outperform those that don't have these over the long run.

A decrease in inventory and accounts receivable leads to good performance.

If a company pays a good amount of taxes, usually their returns are higher than those who don't.

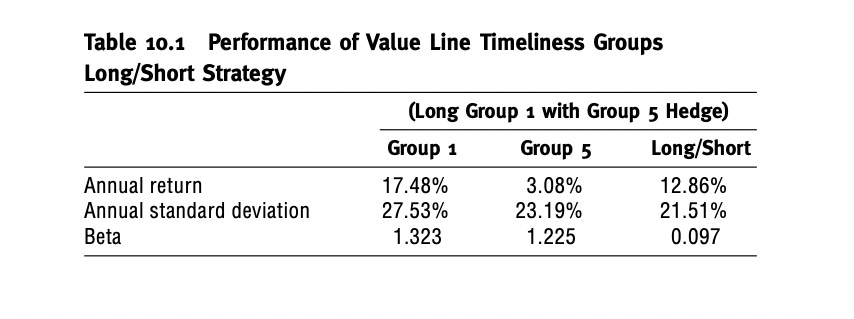

Value Line

One of the things he noted is that the Value Line Timeliness Group 1 and the Technical Analysis Group 1 outperformed the Group 5 significantly. A long-short strategy of buying Group 1 and shorting group 5 makes money in 75% of the quarters.

Luckily a friend was so nice to send me the current value line. So here are the stocks that are Ranked Group 1 in timeliness and technicals and the ones that are group 5 in both. I am not sure how valuable this strategy is, given that the book came out in 2003, but I find it interesting nonetheless.

Timeliness + Technicals in Group 1

Untimely stocks Ranked 5 in technicals and timeliness.

The Shitco Index

I found a cool article about companies. It is an index that is invested in the worst companies out there. Where most of them will go bankrupt, some of them will no doubt be winners. I will look through them next time.

Future of the Newsletter

A few people have asked me if I will put my writing behind a paywall. The answer is no. The reason is that I write mostly for myself. I would hate having to deliver a specific quota per week or month. Sometimes, I just don't find anything, or I am not interested in writing down more than a short Tweet. . What I have found tho, is that my writing productivity is proportional to the amount of Thai food I consume from my favourite restaurant, so I might add a paid tier to support my Thai consumption, but the articles will always remain free.