Hello,

Long time no see. I have not written for some time now with the Omaha visit, another holiday, the nice weather and me mixing/recording a song for my metal band. In Omaha I attended many events and met great people. To make a long story short - it was awesome. I thoroughly enjoyed talking with most people and the side events were more fun than the actual Berkshire AGM. If everything works out, I hope to attend again next year.

Short thoughts

Looked at DOCS.L and FEVR.L during the flight to the US. While decent companies, both are too expensive given the risks in apparel or the implied growth rate of Fever Tree in the valuation. Dr Martens declined 30% since I have looked at it and now looks quite interesting. Had my fair value at around 1b market cap.

Analysing culture is useless in my opinion. Culture is a result of the business model not vice versa. As the business model changes, so does the culture

Gabelli hosted an event in Omaha, so I had a look at their stock. Gamco Investors is quite expensive and should be at around 350m in market cap given their AUM.

Games Workshop (GAW.L) is an excellent company, but vastly overpriced in my view. Would buy it with a market cap of 1.8b, not at today's prices, which is nearly twice that. The reasons for my conservative valuation is the already excellent monetized fan base and competition from cheaper brands and 3D-printing.

Petrobras confirmed a dividend of $0.76/share for Q1. A 7.5% payment for a single quarter. That is quite a bit better than my conservative estimate of 18% for the full 2023. I still think the company is cheap there and plan to reinvest the dividends.

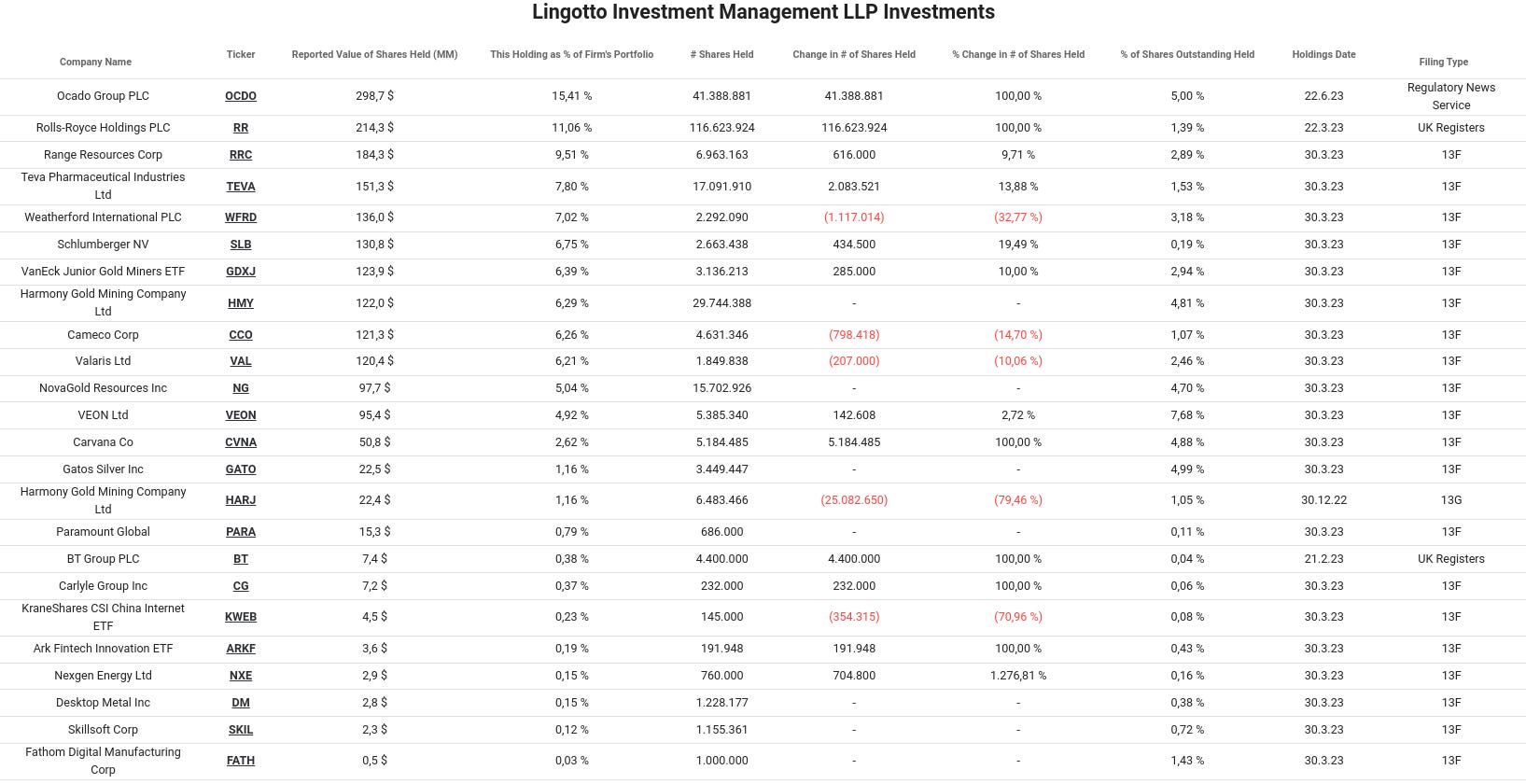

Exor's public portfolio

One of the most fascinating companies is Exor. With Elkan being the CEO they own part of Stellantis, Ferrari, Juventus, CNH, Institut Merieux,Iveco, The Economist and a bunch of other companies with a great track record.

In their last letter the CEO highlighted Matteo Scolari, who previously worked at Eton Park as a hedge fund manager, and took over the public investment fund of Exor in 2015. Since then he managed a 19% annualised return with no down years. Impressive.

Sadly we only know a small part of his portfolio. According to the annual report, their biggest positions should be in Gold miners. If those or other holdings are outside the US and they don't own more than 5% of the company - we will never know the position. Despite that, those that we do know, are exceptionally interesting.

It seems that they invest into certain themes or factors (Gold, Innovation, Uranium), when they hit deep value (like Valaris that they owned nearly directly after bankruptcy) or that have reached sentiment bottoms. Those sentiment bottoms are usually traded quickly, with deep value being held longer.

I will try to find out more about their investment style.

Wading through the Austrian Stock Market

I have recently looked at the stock market from my home country: Austria. At first glance the market looks cheap, given that Austria is around the 30th largest economy in the worth with the 12th highest GDP/capita, and a Shiller PE of 11. However on a closer look it becomes clear why. Companies bogged down by bureaucracy and a big exposure to Eastern Europe and Russia.

I went through all companies with their primary listing in Austria or that are from Austria, but are listed somewhere else and read each and every single annual report. I did it to challenge myself, but it can only be described as investor masochism. Despite only finding two companies that I would buy at today's prices - and not a single one I actually bought (due to having too much exposure to oil already), I learnt a huge amount. For example, I hate analysing banks and insurance companies, and that I would only buy them when they are outrageously cheap (like Fairfax a few months ago at 0.6 P/B). There is no visible process in my investing prowess and that can be frustrating. Combined with my stagnant portfolio - it is an exercise in patience and persistence. It is amazing how little process you see, for reading more than 80 annual reports.

I don't want to leave you hanging tho. There are several companies that are very interesting even tho I would not invest in them at current prices, or because they don't offer a big enough discount - that could be interesting for an investor with a different approach than me.

Telekom Austria: A super stable cable/mobile provider company that is not too expensive and has a potential value unlock by creating a spinoff for their mobile towers. Returns are probably decent, but too little torque for my taste.

Erste Bank: Decent numbers, with low growth and a stable customer base. It doesn't clean my hurdle rate, but if I were able to retire tomorrow, I would probably own it.

OMV: Was one of the companies, I would actually buy at this level. However I have enough oil exposure in my portfolio already, and I see Petrobras as the company with more potential upside due to the historic discount compared to their own valuation.

Mayr Melnhof Karton: This is probably the best managed public company in Austria. The price has come down significantly in the last few months. It is still a bit too expensive for me, but I can see it doing decently over the next decade.

Schoeller-Bleckmann is the second company I would buy at those levels. But as it is another oil exposure, I pass.

That is it from me. I am currently working on the company Focusrite and an overview of the whole audio production space (including private players) and on looking at companies that produce or distribute anime. So subscribe if you want to read that.