Hello,

today I am just writing a short article. If you enjoy these shorter thoughts as well - please let me know!

Ben Graham and the GEICO dilemma

Just as I am working through the newest edition of Security Analysis, slogging myself through the fixed income portion in order to understand more how the economics of bonds work, I saw an argument against the philosophy.

Ben Graham made more money with GEICO than all his other investments combined.

In contrast to the article, in my opinion this is by design of the philosophy. Value Investing strives to lower the business risks of operations, and maximising the return by buying cheap and with enough margin of safety. Great opportunities are rare, so most of the companies one is buying with the strategy are not of the highest quality. But sometimes they are.

Businesses are constantly evolving, so given the diversification of Graham's approach companies will turn around. Graham doesn't tell you to sell great companies. If a stock thus improves fundamentals as well, there is often no reason to sell it unless it is at a high premium. By using Graham's value investing approach one makes sure to not make moonshots, but instead let the companies prove themselves to the portfolio.

At the same time the returns through mean reversion and sentiment have proven to be excellent throughout history. The GEICO argument then is an endorsement of Graham's approach - not a detraction.

Update on Unity

John Riccitiello, who was responsible for the licensing mess is stepping down as CEO and is replaced by James Whitehurst, who was CEO of Red Hat since 2007 until the acquisition by IBM for $34 billion. The market approved and the stock bounced more than 6% moments after the announcement. That move was not to last though.

The stock fell and even closed down red, a sign that while the CEO change might be the best for the company, it can't make up for the lost trust of hundreds of game developers and studios. With the stock down over 20% in just over a month, the easy picking have been done.

Macro like Druckenmiller

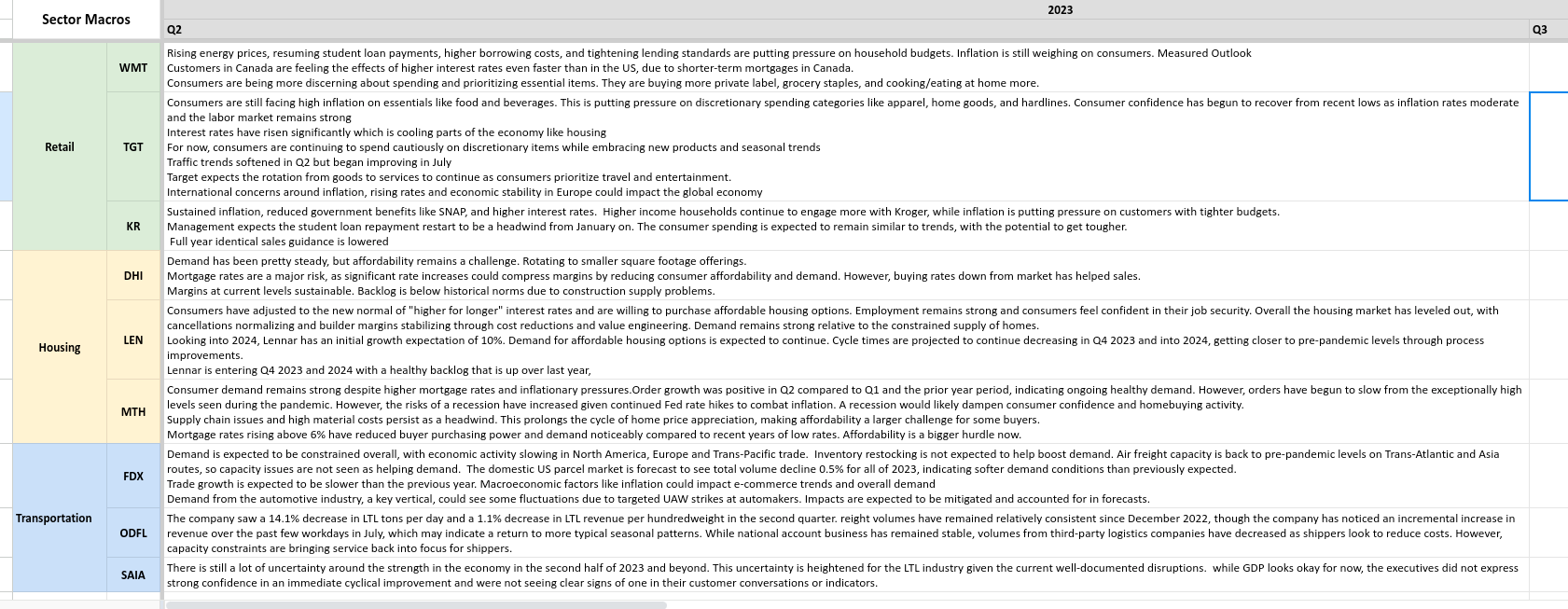

Stanley Druckenmiller is among my biggest investment icons. In contrast to Buffett his investment style does depend on macro economics and that while mostly ignoring most common economic indicators. While he is surely aware of all the latest macro data, he said that they prefer a bottom up approach. Looking at the investment calls of companies in housing, trucking and retail and then extracting information about the next 12 to 18 months.

In order to replicate that, I finally found a workflow that automatically summarises earnings calls for me and extract information about customer outlook, macro data and the outlook of the company itself and throws that into a database. I copy the text and remove duplicate information form the same company. Looks pretty good no?

Cheap banks in emerging markets (and the UK)

A banks earnings potential is dependent on the combination of its book value and the return on equity. Return on Equity looks best when the economy is booming. It ignores downside risk.That is why I focus on book value and add a big margin of safety on top of that. One is betting, that things don't get worse.

I haven't done any deep research into the companies themselves, but here are a few banks that look interesting and trade below 0.8x P/B often significantly so. If you have any research into those companies, I would appreciate if you could link it to me.

Halyk Bank: Bank in Kazakhstan

Bancolombia: Bank in Colombia, Panama, El Salavador, Puerto Rico and Peru.

Postal Savings Bank of China: Chinese bank with low exposure to the real estate problem.

Lloyds Bank looks very cheap here at 0.63x P/B

Banco de Brasil. A Brasilian bank that is up 65% YTD, but still pays over 10% dividend and has excellent ROE.