'This piece is an opinion and for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.'

Good Monday everyone!

I have switched my opinion from anti-nuclear to pro-nuclear a few years ago. However, the stocks were only a quick trade, as I thought it could take decades for the bull thesis to play out. That changed last week.

As many mines have shut down after the Fukushima incident, the sector went into a bear market. As a result, the supply side is now in a structural deficit. The world's power reactors require around 67500t of uranium each year, while the world produced just 48332t in 2021. A deficit of 19168t yearly. However, the high inventory levels hindered the price appreciation of Uranium. The exact inventory levels are impossible to predict due to confidentiality, but the World Nuclear Association estimated 282 000 tU at the end of 2020. Inventory levels thus would be sufficient for close to 15 years, despite the inherent supply deficit.

Despite Japan restarting some of its reactors and China vowing to expand their nuclear reactors, it wouldn't be enough to warrant an investment. However, there is another critical part: the Sprott Physical Uranium Trust. In 2021 Sprott took over what used to be called the Uranium Participation Corp and created the Physical Uranium Trust. The trust issues shares if it trades above the NAV (Net Asset Value) and then buys more physical Uranium. It now holds trust now holds 59.7 million pounds or about 45% of annual production. In 2022, the trust acquired 18 million pounds U3O8. 1t of Uranium is the equivalent of 1.17924t of U308. That means that the world inventories are the equivalent of 332545.68 tU308 and the yearly deficit 22603.672t. If we assume the trust acquires another 18 million pounds U308 (6925.7t) in 2023, that yearly deficit increases to 29529.37 and the remaining inventory to 11 years. Furthermore, Yellow Cake (another trust listed in London) and a new entity backed by Kazatomprom will also acquire physical Uranium - increasing the deficit even more. Thanks, @quakes99 for so much infos on the topic.

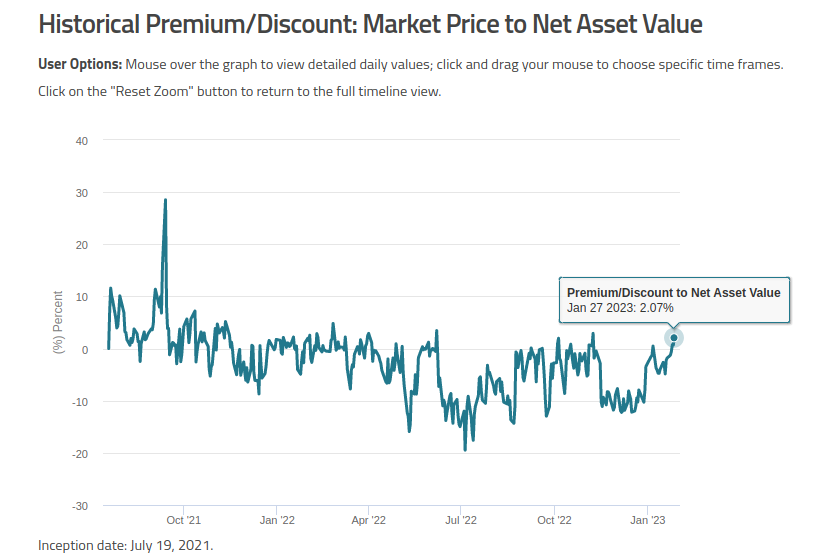

The problem was that the Sprott Physical Uranium Trust often doesn't trade at a premium to NAV. It could take years until they acquire enough Uranium for the market to care. It needs a catalyst.

Theory of reflexivity

The theory of reflexivity created by George Soros is relatively simple. It says that market prices distort the underlying fundamentals and changes them. Furthermore, he believes in positive reinforcements. Forces that accelerate a trend both to up - and the downside, explaining the boom/bust cycle in sectors and the economy.

One example that he gives was the conglomerate boom of the 1960s. Big companies started to acquire undervalued companies with bonds, debentures or convertibles (often diluting shareholders in the process). That meant that the earnings per share of the companies increased and the price of the conglomerate's stock would go up - making it easier for them to acquire other companies. The market thus reinforced the trend. Acquisitions thus become more and more reckless. As interest rates rose to offset the rising inflation, profits began to decline. The market then realized that the acquisitions were often value destructive in industries that required huge reinvestment. Just as the trend accelerated to the upside, it accelerated to the downside - as now corporations were more bloated and inefficient. Bankruptcies and spin-offs followed.

The same patterns could be observed during the first REIT (Real Estate Investment Trust) boom. Introduced in the 1960s, it took them until 1969 to really took off. Soros published a research report in 1970 saying that because REITs can sell shares at a premium over book value, they would create higher per share earnings for their shareholders. Due to the high yield and the anticipation of per-share earnings growth, investors would bay above book value. The more the premium goes up, the more value the REIT can create. That process would reinforce until the amount of REITs and projects became too much, making everyone to scramble for the exists. REITs would then trade discounted to NAV reversing the value accretion as interest rates increased.

A more recent example is the Grayscale Bitcoin Trust. As the trust was an easy way to get access to Bitcoin, it traded at a premium. This allowed the trust to issue shares and buy more and more of Bitcoin. The price of Bitcoin appreciated, leading to a higher premium for the GBTC and reinforcing that trend. Kuppy made the point that the Sprott Physical Uranium Trust has similar properties and that the switch from Underfeeding to Overfeeding (here is a great explanation of what that is) and hedge funds embracing Uranium after the WEF summit is enough to get the ball rolling. I disagree. These forces are helping the ball accelerate, but the ball was stopped until last week.

Kazatomprom missing production goals

After Sprott spent some time trading discounted to NAV, it is now back at a premium (although only 2% as of 30.01.23). It is great that they can start to buy more Uranium again, but the big news is that Kazatomprom missed its own production goals.

Not only did they miss big on their production goals, they also guided towards lower production in 2023 due to delays and supply chain issues. Kazatomprom now expect around 21000t U compared to the previous guidance of around 23000tU. At first glance, that doesn't look massive, but it would mean that 3% of the global production is missing. This decreases the supply deficit even more, drawing the remaining inventory to 8.5 years until depletion, and that isn't factoring in the Japanese reactors that are getting turned on again. Sprott also now has the money to acquire 440t Uranium. Whereas the ball was standing still, despite supply deficit, a switch from underfeeding to overfeeding and a mindset change - in my opinion the ball got rolling and is accelerating now. (Be sure to read Kuppy's post as well).

As a result, I recently bought some Sprott Physical Uranium Trust (U.U), Cameco (CCJ) and Kazatomprom (which trades in London). The reason for my investments in only those two Uranium Miners is basic: They are the only profitable ones. Kazatomprom just missed their own production, but if the price of Uranium increases, so will their earnings. There are many miners that have great assets, but starting a mine can be difficult - especially in a field that was neglected for over a decade. There is a time and place for more risky juniors - but I rather stay on the safer side. All in all, I think that Uranium offers an enticing risk/reward at the moment.